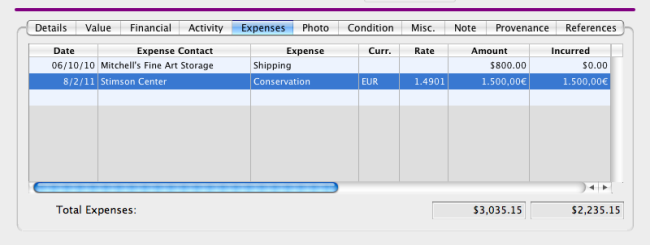

The primary function of the Works Expense Screen is to document all expenses associated with a particular work. Expenses may include costs associated with shipping, framing, restoration, photography, etc. The Expense Screen records both Amount (total amount of the expense) and Incurred Amount (amount which you incurred) of the expense. In cases where another party incurs the expense, add the amount only in amount column (see first entry on image above).

Incurred Expenses added on the Expense Screen are added to the Calculated Net (Calculated Net appears on the Financial Screen, in order to show the overall costs associated with a Work. Incurred Expenses will also affect Net due to Consignor.

button to open the Contact Selection List. Search to find the Contact, and click OK. If the Expense Contact is not in the list, click the Add New

button to open the Contact Selection List. Search to find the Contact, and click OK. If the Expense Contact is not in the list, click the Add New button to add a new Contact.

button to add a new Contact.

The manner in which expenses are entered into the Expenses Screen may affect the database owners overall cost of the artwork including the amount that may be due to the artist/consignor and the gallery’s profit. It is imperative that this information be entered correctly for the financial information to calculate accurately within the program. Below are four examples of how to account for expenses:

EXPENSE EXAMPLE 1

The consignor or artist has already paid for the expense (e.g. framing, shipping, etc.) of the piece in full. The consignor/artist is to be reimbursed a portion or the entire amount of that expense. The expense is actually incurred by the gallery and should be listed as such.

Enter the total amount of the expense incurred by the gallery in the Incurred column. This entire amount will now be added to what is due to the consignor/artist. The financial information for this work will adjust in the Calc.Net and Potential/Profit fields of the Financial Screen in Works.

NOTE: If the amount is split equally and entered equally in both columns (Amount and Incurred) it will adjust the Calc.Net/Potential financial information of the work but the amount due to the gallery will be unaffected. If an amount is split equally it has balanced out and neither party owes the other. This situation may occur if the parties are billed separately and are intending to pay separately.

EXPENSE EXAMPLE 2

The gallery has paid or will be paying for the expense associated with this work in full. The gallery is due the entire amount back. The expense is actually incurred by the consignor/artist and should be listed as such.

Enter the total amount of the expense incurred by the consignor/artist in the Amount column. This entire amount will now be deducted from what is due to the consignor/artist.

EXPENSES EXAMPLE 3

The gallery has paid or will be paying for the expense associated with this work in full. The gallery is due a portion of the amount back. This expense is actually shared by the gallery and the artist/consignor.

Enter the total amount of the expense in the Amount column and enter the amount of the expense that the gallery was/will be responsible for in the Incurred Column. The difference of these amounts will now be deducted from what is due to the artist/consignor.

EXPENSES EXAMPLE 4

The gallery has paid or will be paying for the expense associated with this work in full. This situation applies when the gallery owns the work. This expense is incurred by the gallery alone and will not affect the artist/consignor. The artist/consignor is not associated with this expense at all.

To document expenses incurred by the gallery alone for a particular artwork (when the expenses do not have anything to do with the artist/consignor) enter the total amount of the gallery expense(s) both in the Amount and Incurred Columns. This will adjust the financial information for the gallery’s expenses and potential profit.

Show Accounts enabled

When the Show Accounts is enabled ( see also Preferences) the Account fields appear in the following locations:

Expense: Works>ExpensesTab> Expense view (scroll to right)